Planning & investing terms you should know.

Feel better prepared the next time you speak with a financial advisor or—at the very least—at your next social gathering.

See if our expertise matches with your needs.

Estate Planning

-

Conservatorship is a legal arrangement where a court appoints a person to manage affairs for someone who is unable to do so for themselves.

There are four main types of conservatorships: financial, physical, general, and limited.

-

Estate planning is the process of creating a blueprint for the preservation, management, and distribution of assets in the event of your death and/or mental incapacitation.

This blueprint helps maximize the value and minimize the cost of your estate and ensures a smooth transfer of your assets to heirs.

-

Intestacy occurs when someone dies without a will. In such a situation, a court decides how to distribute their assets.

-

This is a key document that ensures an estate is settled in the manner the deceased had intended. More specifically, the document communicates your final wishes in regards to how assets and other possessions are distributed following your death.

-

A living trust is a legal document in which your assets (anything of value such as a business, real estate, bank accounts, etc.) are placed into a trust account. The trust is set up while you are still living (and personally named the “grantor”). A designated person called a “trustee” is tasked with the responsibility of managing assets for the benefit of the eventual beneficiary or beneficiaries.

There are two types of living trusts: revocable trusts and irrevocable trusts.

A revocable trust is the most common type of living trust. Just as the name implies, a grantor can change (or cancel) a revocable trust at any time. Conversely, nobody—not even the grantor—can change an irrevocable trust. When a grantor passes, the revocable trust automatically converts to an irrevocable trust.

One of the biggest benefits of setting up a trust is that it fosters a smooth transfer of your estate.

-

While the name of this document varies by state, its purpose remains the same: allowing you to specify your end-of-life medical care decisions in the event you are unable to personally communicate them. This document also helps prevent confusion and/or disagreements, as no other party can override the decisions you’ve already made.

A living will may seem similar to a power of attorney for healthcare. While some states combine the two documents, their purposes are different. A living will reflects decisions you’ve made ahead of time, while a healthcare power of attorney names a person who can make medical decisions in your stead if you are unable to.

-

This is a document that gives the party of your choosing the power to make legal decisions on your behalf when (and if) you ever become incapacitated or can’t act on your own behalf.

A power of attorney can take shape as various types and reflect a range of responsibilities. For example, you can set up a power of attorney to permit another party to act only for limited purposes—such as signing loan closing documents in the event you are unable to.

-

Probate is the legal process used to administer a person’s estate after his or her death. This includes verifying that your will is valid and authentic, paying off any taxes or debts, and ensuring the correct parties receive all property and possessions.

Healthcare & Medicare

-

This is a Medicare Part D coverage gap whereby you’re responsible for paying a certain percentage of your prescription drug costs.

-

A health savings account (HSA) is a type of savings account you can use to pay for qualified out-of-pocket healthcare expenses, including deductibles and copays. These accounts are designed specifically to help people with high-deductible health insurance plans (HDHP) pay for such expenses.

-

IRMAA—which stands for “income-related monthly adjustment amount”—is the additional amount (a surcharge on top of Medicare premiums) charged to higher-income beneficiaries.

-

A Medigap plan (also known as a Medicare Supplement plan) is an insurance product designed to reduce—or even eliminate—most out-of-pocket costs associated with Original Medicare.

Medigap policies are standardized, as required by the federal government, regardless of which insurance company sells them. This means companies can only offer policies from a list of about ten standardized plans, each simply assigned a letter: A, B, C, D, F, G, K, L, M, and N. It also means a Medigap plan with a given letter will offer the exact same benefits no matter where you purchase it (with the exception of Massachusetts, Minnesota, and Wisconsin, which standardize their policies differently).

-

Medicare Advantage plans, also known as Medicare Part C, are insurance products offered by private companies approved by Medicare.

The biggest benefit of joining a Medicare Advantage plan is the additional coverage for services Original Medicare doesn’t cover.

-

Our country’s Medicare program consists of four parts (A, B, C, & D) that each cover specific services.

With Medicare Part A and Medicare Part B (also known as “Original Medicare”), the government pays providers directly for services received by a patient: covering patient care in a hospital or skilled nursing facility, in-home hospice, and limited home healthcare services (Part A) as well as medical services and supplies necessary to treat health conditions (Part B).

Insurance

-

An annuity is a type of insurance product that provides investors with a guaranteed income stream. You pay money up front (in a lump sum or series of payments), which is then invested and later paid out at an agreed-upon time—at an agreed-upon amount and timeframe.

-

Long-term care (LTC) is defined as help you may need with “activities of daily living” (ADLs) due to injury, health, or cognitive impairment from dementia, memory loss, or Alzheimer’s. Such activities include bathing, dressing, eating, toileting, continence, and transferring (walking or moving oneself from a bed).

LTC policies work similarly to mortgage and auto insurance policies in that you pay premiums—typically for as long as the policy is in effect—and make claims should you ever need covered services.

-

Term life insurance is the simplest, most affordable form of life insurance. Term life spans a specific amount of time—often up to 30 years—and typically pays your designated beneficiary only if death occurs during the term (your beneficiary will not receive any benefit should you outlive the policy). The death benefit can be paid out as a lump sum, monthly benefit, or as an annuity.

-

Universal life policies (also called “adjustable life insurance”) are another permanent life insurance policy type—offering a higher degree of flexibility than whole life policies. This results from the fact that you may be able to adjust death benefit amounts and apply the money accumulated in the savings component toward your premiums (assuming there is enough money in the account).

For example, let’s say you lose your job and want to save money via less expensive premiums. In this case, you may be able to reduce your death benefit without the need to obtain a new policy. The opposite also holds true, providing you with the potential ability to increase your death benefit without the need for a new policy. The savings component within these types of accounts generally earns a money market rate of interest.

Rather than pay policyholders a money market rate of interest, some universal life policies tie the cash value component to the performance of a stock market index: such as the S&P 500 or NASDAQ 100. These are referred to as “indexed universal life insurance” policies. Guaranteed universal life insurance (GUL) policies also exist and behave similarly to term policies in that the term ends whenever the policy matures (no matter your age). However, these policies allow you to select coverage per a specific age rather than a specific term of 15, 20, or 30 years.

-

Variable life insurance policies resemble whole life policies but differ in that you can decide how you want to invest their cash value component. In doing so, you can invest in a variety of options—including stocks, bonds, and money market mutual funds—that can help increase (or reduce) the value of the savings component within your policy.

With variable universal life insurance policies, you ultimately enjoy the features of both a variable and universal life policy.

-

Whole life is the most common permanent life insurance policy type. These policies offer a guaranteed death benefit irrespective of when you pass away, and your premiums stay fixed. They also include a cash value component—funded from a portion of your premium payments—that often offers a guaranteed rate of return.

Investing

-

Think of a bond as your decision to provide a company or the government with a loan. The entity borrowing the money promises to pay back the loan at a future date (the “maturity” date) and pay interest (via a fixed rate), known as the “coupon” rate. There are many types of bonds, and they are all assigned different ratings based on their credit quality—the higher the credit quality, the less risky the loan.

-

Capital gains are any profit you make when selling an asset such as an investment—like a stock or bond—or perhaps a home or business. The IRS taxes individuals on capital gains in specific circumstances, known as a “capital gains tax.”

Furthermore, capital gains can be broken into two categories: short-term (assets you’ve sold after holding them for less than a year) and long-term (assets you’ve sold after holding them for more than a year). Short-term capital gains are taxed as ordinary income, while long-term capital gains are generally taxed at 15%—provided that your income falls below certain thresholds.

-

A share of common stock represents a piece of company ownership.

When you own at least one share, you are considered a shareholder of that company. As a shareholder, you enjoy voting rights on corporate policies as well as the ability to elect the organization’s board of directors.

-

A dividend is a payment a company makes to its shareholders. Think of it as a bonus or reward you receive for owning the stock.

A dividend is paid per share of stock. For example, if a company pays out $0.50 per share of stock and you own 100 shares, you’ll receive $50. Generally speaking, dividends are paid regularly—often quarterly—but not all stocks pay them out. Companies can also reduce or eliminate these at any time.

-

The DJIA is one of the most well-known and widely followed stock market indices in the world: serving as a barometer for the overall health of the U.S. stock market and, by extension, the economy. The Dow tracks the performance of 30 large, publicly traded companies based in the United States.

-

If you are keen on the performance of a market index—like the S&P 500—but don’t want to spend money buying each individual index stock or dedicate the time to research and manage these, an ETF allows you to replicate index performance at much less expensive rates.

Therefore, we can define an exchange-traded fund as a type of financial instrument that contains a basket of securities (such as stocks, bonds, currencies, and commodities) and often tracks to an index such as the Dow Jones or Nasdaq Composite.

In many ways, ETFs are very similar to mutual funds since they both allow you to invest in a diversified portfolio by purchasing just one security. The primary differences between ETFs and mutual funds, however, exist in how they are managed.

-

An index fund is a type of mutual fund that allows investors to invest in an index such as the S&P 500, Dow Jones Industrial Average (DJIA), or more specialized indexes that track a specific industry or segment. Index funds are designed to mirror the returns of that specific index and do not offer fund managers, which is why they are usually a cost-effective investment.

-

A mutual fund is a type of fund that pools money from various investors to purchase securities. Investors buy shares or units in the fund, which are then invested and managed by a professional portfolio manager.

Mutual funds are often comprised of stocks, bonds, and short-term assets such as money market funds—or a combination of the three. Assets within the fund are called “holdings” and vary based on fund objectives. For example, a riskier small-cap fund may reflect only smaller company stocks, while large-cap mutual fund holdings will include large company stocks.

Mutual funds are popular among investors since they offer an easy way to diversify and spread risk across several investments.

-

The Nasdaq—short for the National Association of Securities Dealers Automated Quotations—is one of the largest stock exchanges in the world, home to over 3,000 publicly traded companies.

Although the exchange is indeed associated with the tech industry, it also includes companies from other sectors such as healthcare, consumer goods, and financial services.

-

The P/E ratio is a tool used to calculate company worth.

More specifically, it tells you how much money you are paying for $1 of the company’s earnings. For example, if a company is reporting a profit of $5 per share and each share sold for $20, the P/E ratio equals 4—meaning the company is trading at four times its earnings.

This ratio is compared to others within the same industry or to past ratios posted by the same company. While there is no rule dictating what a “good” P/E ratio is, the average historic median P/E for the S&P is almost 15.

-

Like common stock, preferred stock also represents a piece of company ownership.

One of the biggest differences between the two is that preferred shareholders usually have no voting rights. However, preferred stockholders do enjoy access to more benefits than a common stockholder. For example, not only does preferred stock pay a higher dividend rate than common stock issued by the same company, but the issuer must pay out preferred stock dividends before any common share dividend is paid out. In addition, preferred stockholders rank higher than common stockholders in the event of liquidation.

-

Real estate investment trusts are companies that own, operate, or finance income-producing real estate across a wide range of sectors: including apartments, hotels, shopping malls, office buildings, and warehouses.

Typically, a REIT collects money—such as rent from tenants or interest from investments—and then distributes that money as dividends to shareholders. Many real estate investment trusts are publicly traded on major securities exchanges, and investors can therefore buy and sell them like stocks. As a result, REITs allow any investor to earn income produced from real estate without the need to own or manage properties.

-

The S&P 500, or Standard & Poor's 500, is a stock market index that measures the performance of 500 of the largest publicly traded companies in the United States.

-

A stock split occurs when a company increases the number of its outstanding shares by offering additional stock to current shareholders, thus lowering the price per share.

For example, if a shareholder owns 10 shares of stock worth $100 ($10 per share) and the company decides to move forward with a 2-for-1 stock split, the shareholder will then own 20 shares of stock worth $100 ($5 per share) after the split.

Retirement

-

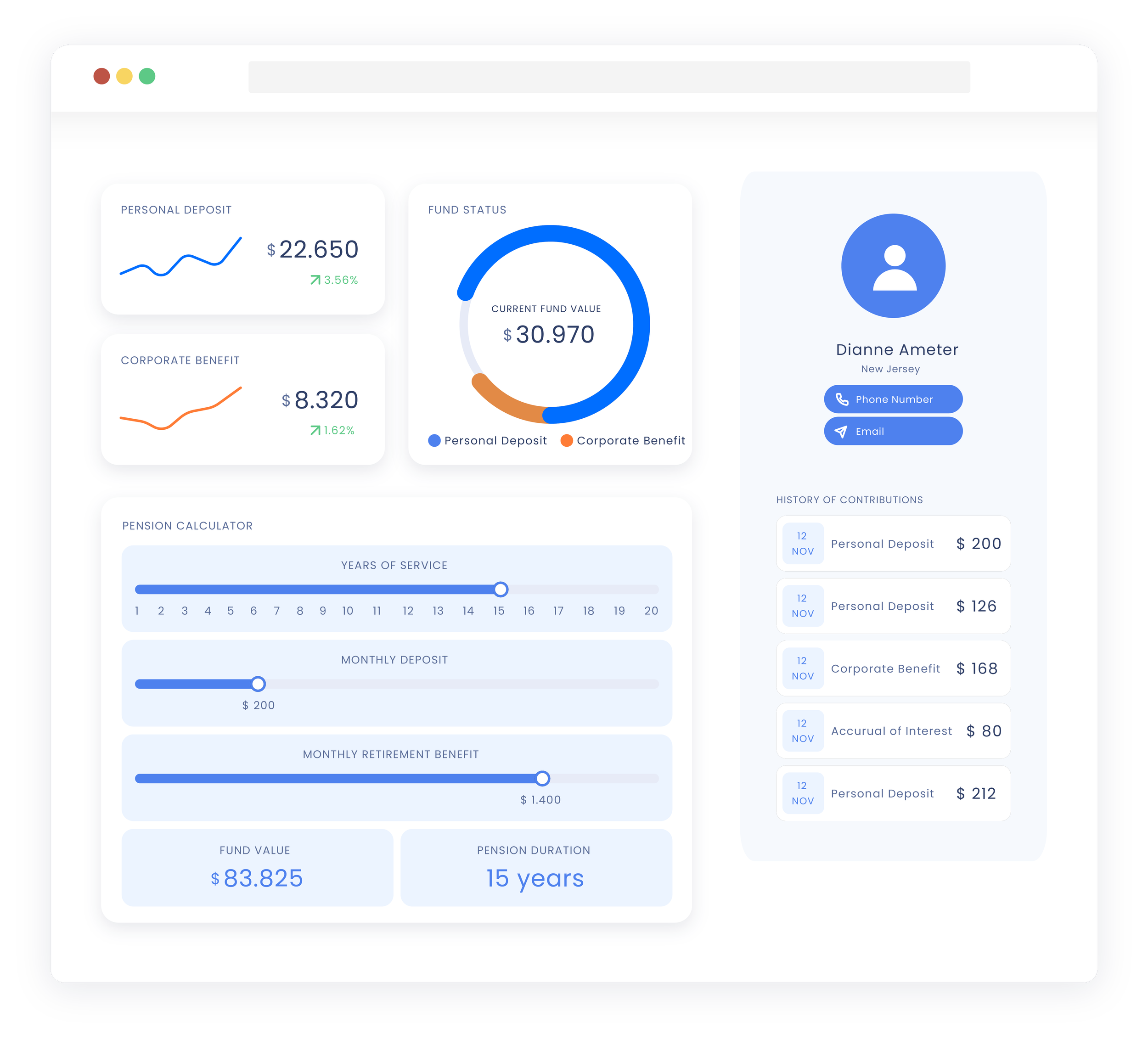

A traditional 401(k) is a type of retirement account that is employer-sponsored. Employees who wish to participate can invest a percentage of their pretax income (from their paycheck, on an automatic basis) to fund their 401k accounts. As an added benefit, most employers match employee contributions (up to a certain percentage), which is essentially “free money” for the participating employee.

-

This retirement plan is similar to a 401(k) but only offered to nonprofit organizations.

-

A backdoor IRA isn’t a type of retirement account—it’s an IRS-approved method for those with high incomes to fund a Roth IRA even though their income is higher than IRS thresholds.

-

If you’re 50 or older, the IRS established rules to help you save more money for retirement via “catch-up contributions”: additional contributions you can make to your 401(k) and IRA accounts above the standard limits.

-

When you change jobs, you can either leave your money in your current employer’s 401(k) plan, cash out your savings, or roll over the funds into your new employer’s 401(k) or an IRA.

-

A mega backdoor Roth is a retirement strategy that allows higher-income earners to save more money for retirement.

-

A QCD is a direct transfer of funds from your IRA—payable directly to a qualified charity—often used by investors who want to avoid being pushed into higher income tax brackets or to prevent the phaseout of other tax deductions.

-

Required minimum distributions (RMDs) is the minimum amount of money the IRS requires you to withdraw from specific retirement accounts: primarily tax-deferred accounts, such as traditional IRAs and 401(k)s, and generally beginning at age 73.

-

An IRA is a savings account specifically designed to help fund your retirement. You can invest in diverse types of assets within the account, including stocks, bonds, ETFs, and mutual funds. There are many types of IRAs, with traditional and Roth IRAs as the most common.

A Roth IRA offers valuable tax benefits, and your contributions are funded with after-tax dollars. Therefore, your money can grow tax-free and offer you tax-free withdrawals on qualified distributions in retirement.

-

A Roth IRA conversion is merely a transfer of all (or a portion) of your balances from an existing traditional IRA, SEP, or SIMPLE IRA as you roll the assets over into a Roth IRA.

-

The "five-year rule" states that you must own your Roth IRA account for at least five years to make tax-free withdrawals from the earnings portion of the account (you can withdraw sums equivalent to contributions you've made both penalty and tax-free—anytime and for any reason).

Once the 5-year rule has been met, and you are 59½ or older, you can withdraw from the earnings portion of your account without taxes and penalties.

-

An SDRIA is an IRA account that offers greater flexibility with respect to types of assets you can invest in. These accounts are also managed by the account holder rather than the financial advisor or firm.

-

SEP IRA accounts are a type of tax-deferred retirement savings plan used to provide retirement benefits for business owners and employees.

Generally speaking, SEP IRAs are geared toward small businesses (or people who are self-employed) with zero or few employees and want the flexibility to choose when and how much to contribute.

-

Like SEP IRAs, SIMPLE IRA accounts are a type of tax-deferred retirement savings plan used to provide retirement benefits for business owners and employees. However, unlike SEP IRAs, these are typically geared toward larger businesses of up to 100 employees.

-

As stated above, an IRA is a savings account specifically designed to help fund your retirement. You can invest in diverse types of assets within the account, including stocks, bonds, ETFs, and mutual funds. There are many types of IRAs, with traditional and Roth IRAs as the two most common.

A traditional IRA is a tax-deferred account, meaning you pay taxes at a later date. Therefore, any contributions you make are typically funded with pre-tax dollars, and earnings grow in a tax-deferred manner until you withdraw them in retirement.

Social Security

-

The Social Security Administration (SSA) is required by law to prevent inflation from eroding the purchasing power of benefits paid to recipients. They do this via COLA, or cost-of-living adjustments, which are automatic benefit amount increases initiated by the SSA.

-

When you apply for Social Security, the SSA decides if you will receive benefits. They’ll send you an official letter explaining their decision and, if benefits are payable, will tell you the amount you will receive each month.

-

You can start receiving Social Security retirement benefits as early as age 62 (early retirement age) for workers (or age 60 for widows or widowers).

-

You can begin receiving Social Security benefits at the age of 62. However, you won’t be entitled to 100% of your benefits until you reach your full retirement age (FRA).

This number is based on your birthdate; if you were born after 1960, your full retirement age is currently 67. Knowing this age helps determine the overall impact of any post-retirement employment on your Social Security benefits.

-

Under a special Social Security Administration rule that applies for one year—typically during the first year of your retirement—you can receive a full Social Security check for an entire month of retirement, regardless of yearly earnings.

This rule was created so as not to penalize people who retire mid-year (or later on in the year) and have already earned more than the pre-retirement earnings limit.

Tools & Strategies

-

Simply put, asset allocation is how you divide your investments among different assets—such as stocks, real estate, and cash. The percentage by which to divide your assets is driven by your tolerance for risk, time horizon (period between your initial investment and when you’ll need the money), and goals. Therefore, asset allocation is unique to every individual investor.

-

Diversification—a strategy used to help minimize investment portfolio risk—is often achieved by allocating your investments among different types of assets and sectors within both domestic and foreign economies.

-

Dollar-cost averaging is a long-term investment strategy that entails spreading out your equity purchases (stocks, funds, etc.) over regular buying intervals and in roughly equal amounts—rather than as one lump-sum purchase. For example, rather than purchasing $24,000 of a stock in one shot, you’ll buy $1,000 worth of shares (of that same stock) every month over a 24-month period. The objective of dollar-cost averaging is to minimize the risk of market volatility, smoothing your purchase price over time to avoid investing all your money at the pinnacle of the market.

-

Rebalancing is simply the act of adjusting (buying and selling) your investments to restore portfolio weights to your desired asset allocation.

For example, assume your initial portfolio value was $50,000 and your financial advisor initially allocated $30,000 (60%) to stocks and $20,000 (40%) to bonds. Then, assume these stocks do really well over the year and the overall value of your portfolio increases to $55,000 but also shifts your allocation to 70% stocks (worth $38,500) and 30% bonds (worth $16,500).

Your financial advisor would simply sell stocks and buy additional bonds to return to your portfolio's original 60/40 allocation. Ultimately, rebalancing is done to help optimize your portfolio.

-

Risk tolerance is defined as your ability and willingness to stomach large swings in the value of your investments.

Your financial advisor will typically offer you some sort of risk tolerance questionnaire that asks several questions about various market scenarios. For example, what action (if any) would you take if the stock market fell by 15% over a six-month period?

These responses help your financial advisor determine how to best allocate your money based on how comfortable you are with risk. For example, the higher the risk tolerance, the more likely it is that your portfolio will include riskier investments such as stocks. A lower risk tolerance could mean more stable investments in your portfolio: such as bonds or certificates of deposit (CDs).

These responses help your financial advisor determine how to best allocate your money based on how comfortable you are with risk. For example, the higher the risk tolerance, the more likely your portfolio will include riskier investments such as stocks. A lower risk tolerance could mean more stable investments in your portfolio, such as bonds or certificates of deposit (CDs).

-

Short selling is a speculative investment strategy where an investor borrows shares of a stock or asset he or she believes will decrease in value. The investor also promises to replace the borrowed stock or asset in the future. From there, the investor then sells these borrowed shares to a buyer willing to pay the market price before repurchasing them later—ideally at a lower cost than what they were sold for.

-

Tax-loss harvesting is a tax-mitigation strategy that allows you to sell investments that have decreased in value to offset the amount of capital gains tax owed from selling profitable assets. You can deduct up to $3,000 from your taxable income when capital losses exceed capital gains. And if your losses exceed $3,000, the remaining amount can be carried over and deducted from your tax returns in future years until you’ve used up the entire amount.

Types of Financial Advisors

While there are some very clear distinctions between each type of financial advisor, know that overlap can exist between roles. For example, many financial planners will also offer investment advice and management services in addition to planning expertise. For more information on how to choose a financial advisor, click here.

-

If you’re looking to merely buy and sell securities such as stocks and bonds, you’ll need a broker: which is essentially an intermediary between an investor and a securities exchange. You can choose between full-service brokers such as Morgan Stanley, Stifel, and Merrill Lynch and discount brokers including E-Trade and TD Ameritrade. While discount brokers charge lower fees and commissions, their scaled-back service means you’ll have to make investment decisions on your own—whereas full-service brokers provide personalized investment advice.

-

A fiduciary financial advisor is a financial professional who is legally and ethically bound to act in the best interests of clients. Unlike other financial advisors who may operate under a "suitability standard”—meaning they must recommend products that are appropriate for a client’s needs—a fiduciary is held to a higher standard of care. This responsibility means they must prioritize their clients' interests above their own and disclose any potential conflicts of interest that could affect their recommendations.

-

This segment of financial advisors offers a much broader service offering than just investments alone, integrating all components of your financial life—including savings, insurance, and taxes—to fulfill your short-term and long-term aspirations.

-

Simply put, this category of advisors provides clients with advice on their investments and manages their investment portfolios for a fee. While this option is more expensive than a robo-advisor, you’ll receive much more personalized service and access to a wider breadth of investments.

-

Also known as automated investment advisors, these are online platforms that provide investors with computer-generated financial planning and investment services. Betterment and Wealthfront are two of the most popular examples (we also partner with Betterment for our VR Robo solution). Robo-advisors are best suited for novice investors who don’t have a lot to lose, investors who merely have some basic investment management needs, or investors looking to pay as little as possible (robo-advisors are relatively inexpensive). Some of these platforms also provide access to a “human” financial advisor.

-

Essentially, this segment represents a hybrid of both investment advisors and financial planners; but they often primarily serve high-net-worth and ultra-high-net-worth clients.

Other Terms to Know

-

In its simplest terms, financial planning is the process of planning and managing your short and long-term finances to help achieve your financial goals and desires—both during your working years and after you retire.

This includes seven components: 1) establish long and short-term goals 2) protect your assets (through insurance) 3) control your cash flow (budgeting) 4) invest wisely 5) manage your taxes 6) save for retirement and 7) leave a legacy (estate planning).

-

The New Jersey Exit Tax is a misnomer, as many people believe it’s an additional tax or special tax imposed when you sell your property and move out of state.

The truth is that this is merely a prepayment of the estimated tax you owe on the sale of your property, paid in advance (either before or at closing) and held in escrow. The tax is then settled when you file your state income tax return.

-

Retirement planning is more specific than financial planning, focusing on your finances and mental well-being for life after work.

-

A reverse mortgage is a loan that allows homeowners to convert a portion of their home equity into cash. Unlike a traditional mortgage whereby the borrower makes monthly payments to the lender, in this case, the lender actually makes payments to the borrower. That’s why these types of loans are called “reverse mortgages.”

Disclosures:

These terms are a summary only and are not intended to provide specific advice or recommendations for any individual or business.

Start simplifying

your journey and speak to a financial advisor today.

See if our expertise matches with your needs.