How to Minimize Retirement Income Taxes

You can indeed implement a variety of strategies to make retirement more affordable such as downsizing your home, delaying Social Security benefits, or even working part time. Another fine option? Minimizing your tax bill to avoid padding government pockets. This article discusses how to do just that.

Key Takeaways

- Start by calculating your "after-tax" retirement savings; money in a tax-deferred 401(k) or IRA is worth less than the balance shows given income tax owed on every withdrawal.

- Roth IRAs and Roth conversions build tax-free income and tax diversification, with a conversion counting as taxable income in the year it’s performed.

- A tax-efficient withdrawal strategy—knowing how and when to draw from taxable, tax-deferred, and tax-free accounts—can keep you in a lower bracket and stretch your savings.

- Other levers include qualified charitable distributions (QCDs), tax-free municipal and Treasury bonds, holding investments for more than year for the sake of lower capital gains rates, tax-loss harvesting, and HSAs.

- Where you live matters, too; some states tax Social Security or retirement account withdrawals so be sure to compare tax rates before relocating.

9 Strategies to Minimize Retirement Income Taxes

No single move solves it — a combination tailored to your situation does.

Strategy 1

Maximize Roth IRAs

Tax-free growth and tax-free withdrawals after age 59½. No RMDs during your lifetime.

Strategy 2

Roth conversions

Move pre-tax IRA dollars to Roth in low-income years — smooth your lifetime tax bill and shrink future RMDs.

Strategy 3

Plan for IRMAA

Medicare surcharges are based on income from 2 years prior. Plan withdrawals to stay below bracket thresholds.

Strategy 4

Live in a tax-friendly state

State tax treatment varies widely. Some states tax Social Security, retirement income, or have high property tax.

Strategy 5

Tax-efficient withdrawal order

Pull from taxable, tax-deferred, and Roth accounts in the right sequence to manage your bracket year to year.

Strategy 6

Qualified Charitable Distributions (QCDs)

Age 70½+? Send up to $111K/year directly from IRA to charity. Satisfies RMDs without adding to taxable income.

Strategy 7

Tax-free bonds

Municipal bonds = federal tax-free (often state-free too). Treasuries = state and local tax-free.

Strategy 8

Hold investments long-term

Held over 1 year = 0–20% capital gains rate. Held under 1 year = taxed as ordinary income. Use tax-loss harvesting to offset gains.

Strategy 9

Use a Health Savings Account

Triple-tax advantage: deductible going in, tax-free growth, tax-free withdrawals for qualified medical expenses.

Know what your “after-tax” retirement savings looks like

Your 401(k) Balance Isn’t What You Keep

Example: $500,000 in a tax-deferred account, withdrawn at a 32% income tax rate.

On your statement

$500,000

Gross balance in a 401(k) or Traditional IRA

→

After 32% tax

−$160,000

What you keep

$340,000

Real spendable retirement income

Why it matters

Always think in after-tax dollars when planning retirement. The right tax strategy can shift tens or hundreds of thousands of dollars back into your pocket.

Maximize Roth IRAs

When you put money into a Roth IRA, you’re using after-tax dollars to do so (having already paid taxes on that income). The big advantage here? Your investments can grow tax-free; you can make withdrawals without worrying about taxes when you retire, provided you owned the account for at least five years. Many people also invest in Roth IRAs specifically to avoid required minimum distributions (RMDs)—withdrawals required by the IRS once you hit a specific age (73, as of 2023)—since there are no RMD requirements for the original account holder. Your money can therefore continue growing tax-free indefinitely, giving you more flexibility and control over your retirement savings.

Consider Roth IRA conversions

One option, especially if most of your retirement funds are tied up in tax-deferred accounts, is to consider a Roth IRA conversion: the process of moving money from a traditional IRA, SEP, or SIMPLE IRA into a Roth IRA. The main perk of doing so is better tax diversification for retirement account withdrawals (helping you save more money in the long run), but remember that the amount moved counts as taxable income for that same year and can thus bump up your tax bill.

Roth conversion example

Consider a couple, both people 59 years old, with the wife already retired and the husband planning to retire next year at age 60. Assume they will collect SS benefits at their full retirement age (FRA) and have a liquid net worth of about $1.8 million (with a home worth $600k and no mortgage). Current expenses are ~$11k a month—expected to fall to ~$8,100 a month in retirement—and almost all liquid assets are in pre-tax retirement accounts and subject to ordinary income tax upon withdrawal as well as future RMDs.

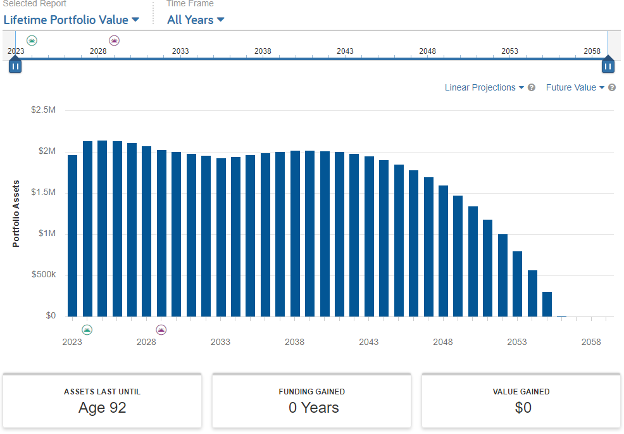

Pre-conversion

Based on the current scenario and assumptions, we can see their portfolio assets will allow them to draw down until each is 92 years old. This also assumes an expected rate of return based on their existing asset allocation, estimated at ~7% based on the level of risk their investments carry.

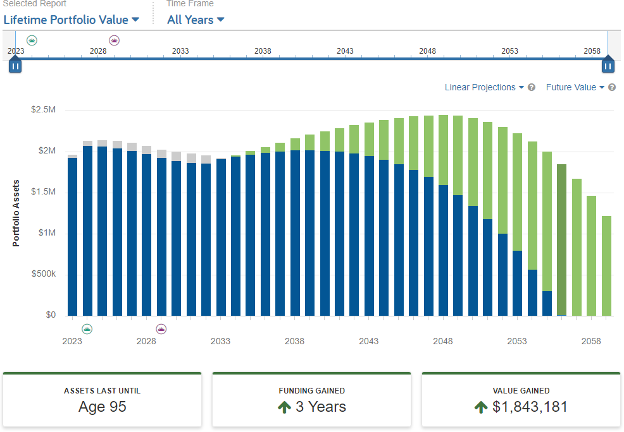

Post-conversion

This scenario illustrates the couple performing a Roth conversion for two pre-tax accounts, totaling about $1.4 million in portfolio value, over a 10-year conversion period.

As you can see, their overall net worth and portfolio value initially decline due to taxes on these conversion amounts. A net increase in portfolio value begins in 2034, however, when Roth conversions cease. In this scenario, we’re assuming a lower expected rate of return due to the clients' older age and lower risk tolerance of 4.87%; despite this, the strategy adds about $1.84 million in net worth to their portfolio over time and allows them to live comfortably beyond age 92 without fearing depleted funds.*

While a Roth conversion doesn’t make sense for everyone, considering it as an option is recommended especially for those with a lot of retirement money tied up in tax-deferred accounts.

Plan for Medicare surcharges

Did you know Medicare charges extra fees to higher-income beneficiaries? It’s true; the more you earn, the more you’ll pay for Medicare Part B and D premiums. These additional charges are referred to as “IRMAA” (income-related monthly adjustment amount) and can add hundreds of dollars to monthly costs and thus catch retirees off guard, but there’s a twist: Medicare surcharges aren’t based on current income and are instead calculated using tax returns from two years prior. For example, your 2026 income determines your IRMAA in 2028, your 2027 income affects your IRMAA in 2029, and so on.

Live in a tax-friendly state

Watch out if you’re relocating

8 states still tax Social Security benefits

- Colorado

- Connecticut

- Minnesota

- Montana

- New Mexico

- Rhode Island

- Utah

- Vermont

Good news for NJ residents

New Jersey doesn’t tax Social Security benefits — one of the bright spots in an otherwise high-tax state for retirees.

When it comes to choosing the best tax-friendly state for retirement, a one-size-fits-all answer doesn’t exist; your ideal state depends on your financial situation including where your retirement income comes from, how much you’ve saved, and what you want to leave behind for loved ones. The state you choose—and your filing status—can have a big impact on your tax bill in retirement, so it’s smart to do your homework before making a move.

For example, those with Social Security as their primary source of income in retirement may want to steer clear of states that tax these benefits—every dollar matters when you’re on a fixed income. Such states include Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, and Vermont, so living elsewhere can help you stretch your retirement income even further.

Don’t forget to consider other state and local taxes that can eat into your retirement savings such as taxes on IRA and 401(k) withdrawals and property/sales tax. Your filing status—whether you’re single or married—also affects your state tax bracket and how much you’ll owe. Every state has its own rules, so be sure to compare tax rates and brackets when deciding where to retire to keep more money in your pocket each year.

Implement a tax-efficient withdrawal strategy

Knowing how much money you can afford to withdraw is a good start, but you’ll also need to know how and when to withdraw from each type of account (e.g., taxable, tax-deferred, and/or tax-free). Doing so can help minimize the amount of taxes you’ll pay out in a given year.

If you pull money from your traditional IRA first, for example, you’ll pay regular income taxes on each dollar withdrawn—whereas you may only be taxed on capital gains and thus stay in a lower tax bracket for a few more years if you pull from your taxable account instead. A Roth IRA can keep growing tax-free, meanwhile, and you can use those funds later on in retirement if you find yourself in a higher tax bracket. Create a personalized withdrawal plan to avoid paying extra taxes, stretch your retirement income, and make your savings last longer. Retiring before 59½ adds a wrinkle: you'll need a penalty-free way to reach those funds early. Our guide to the Roth conversion ladder vs. 72(t) distributions covers both IRS-sanctioned routes.

Keep in mind qualified charitable distributions (QCD)

A qualified charitable distribution (QCD) lets you channel money directly from your IRA to a charity with no detours nor extra steps, with those age 70½ or older able to transfer up to $111,000 each year from a traditional IRA to a qualified charity. Not only does this count toward some or all of your required minimum distributions (RMDs), but the real win happens with respect to your taxes. Unlike standard RMD withdrawals, QCDs don’t get added to your taxable income—so you can sidestep a higher tax bracket altogether—and perhaps still qualify for certain tax credits and deductions or even dodge higher Medicare surcharges or extra Social Security taxes. Using QCDs to keep your taxable income lower can indeed make a real difference when it comes to your retirement finances.

Consider tax-free investments

Municipal bonds—often called “munis”—are issued by cities, states, and other government agencies to pay for big projects such as highways, schools, and airports. The real perk of investing in them is the corresponding tax break since the interest earned is usually exempt from federal taxes; you might even dodge state taxes too if you buy bonds from your own state! This tax-exempt interest can help lower your overall tax bill in retirement, making municipal bonds a smart choice for tax-conscious investors.

Treasury bonds are another solid option if you’re looking for safe, tax-friendly investments. Backed by the U.S. government, they pay a fixed interest rate and typically mature in 10 to 30 years. One big advantage? Their interest is exempt from state and local taxes. That means you can enjoy steady income and potentially reduce your total tax liability, making them a great addition to your retirement portfolio.

Take advantage of tax laws

You can take advantage of the current tax code for your investments and pay less in taxes during retirement, with several ways to do so including:

Holding on to your investments longer

When you're planning for withdrawals in retirement, don't forget about capital gains: profits made when selling investments for more than you paid. These fall into two categories: short-term and long-term. While short-term gains come from investments you’ve held for a year or less (and are taxed at your regular income tax rate), long-term gains come from assets held longer than a year at much lower tax rates (typically between 0% and 20%, depending on your income). Try to hold onto your investments for more than a year if you can, this simple move helping you keep more of your retirement money and pay less in taxes overall.

Using investment losses to offset investment gains

Another smart way to lower your taxes in retirement is by using tax-loss harvesting, a strategy that involves selling investments that have lost value to help cancel out taxes owed on investments that made money. This approach helps you manage your investments, reduce your tax bill, and stretch your retirement income further.

Familiarize yourself with health savings accounts

A health savings account, or HSA, is another worthy investment to consider as you navigate taxes in retirement. HSAs allow you to set aside money for medical expenses on a pre-tax basis (via payroll deductions or using after-tax money and then claiming contributions as a tax deduction during tax time). You can then use these funds to cover deductibles, copays, and other qualified medical expenses.

Several benefits are associated with HSA investments, the largest being the absence of a deadline to use your funds—any money left in your account at the end of each year simply rolls over and remains in the account indefinitely until it is used. Money in the account also generally grows tax-deferred and won’t require you to pay taxes on the same, provided you spend on qualified health costs.

Pay off your mortgage

Housing costs—which include mortgage, rent, property taxes, insurance, maintenance, and repairs—represents the largest expense for retirees. More specifically, the average retiree household pays an average of $22,193 per year ($1,849 per month) on housing expenses, comprising over 36% of annual expenditures. Paying off your mortgage can help save on taxes by potentially reducing the amount you'll need to withdraw from traditional IRAs or other retirement accounts subject to taxes.

In sum: tax-saving steps in retirement

Average retiree household expenses (for households led by someone age 65+) add up to over $61,432 per year, according to the Bureau of Labor Statistics, and will only increase over time. Since every dollar matters, you'll want to make sure you minimize what you pay in taxes accordingly.

Have questions about planning for your retirement? Schedule a free consultation with one of our CFP® professionals to get them answered.

Reviewed for accuracy

Paul Muller, AEP®, CFP®

Founder and Relationship Manager at Vision Retirement, with 30+ years in the financial industry.

Read full bio →

Disclosures:

This document is a summary only and is not intended to provide specific advice or recommendations for any individual or business. Traditional IRA account owners must consider many factors before performing a Roth IRA conversion, which primarily include income tax consequences on the converted amount during the conversion year, withdrawal limitations from a Roth IRA, and income limitations for future Roth IRA contributions. You’re also required to take a required minimum distribution (RMD) in the year you convert and must do so before converting to a Roth IRA.

*This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.