What You Should Know About Credit Scores

Your credit score matters. While you already know lenders use this number to assess your credit risk, you may not know that many companies you likely do business with often check credit scores as well. For example, insurance companies often use this to set premiums for auto and homeowners’ policies, utility companies may use them to assess creditworthiness, and even landlords rely on credit scores to screen potential renters (as timely rent payments is of course a top concern). Now that we know just how essential credit scores are for various parties, we will cover related topics around the same—beginning with credit bureaus.

What is a credit bureau, and how do they collect information?

Credit bureaus are agencies that compile and maintain relevant consumer data and then sell that credit information to lenders and creditors so they can better evaluate the creditworthiness of prospective customers.

While credit bureaus receive customer data from various sources, each relies on lenders and creditors to collect and share their data. Bureaus also obtain data from public records—such as property or court records—to compile a credit profile, which is then consolidated into a credit report made available to businesses and consumers.

In the U.S., three major credit bureaus furnish the vast majority of individual credit reports: Equifax, Experian, and TransUnion. These private companies are regulated by the Fair Credit Reporting Act, and most lenders will defer to their ability to compile credit reports over smaller bureaus (smaller, less established companies do in fact exist).

All three bureaus generally provide accurate credit reports, meaning one isn’t considered more superior to the others.

How are credit scores determined?

Your credit score is determined using information from your credit report, an extensive document detailing your credit history in its entirety including the loans you’ve taken out, your lenders, the speed with which you make payments, etc. It will also include any court proceedings against you that involve your finances, whether you’ve filed for bankruptcy and/or have any federal tax liens claimed against your property.

When assessing a credit score, bureaus typically bear in mind an individual’s payment history and credit utilization: with these two factors accounting for anywhere from 55%–70% of your total score, depending on the bureau and subsequent scoring model.

Your payment history is based on how consistently you pay your bills (and other credit obligations) on time; payments late by 30 days or more are often reported to credit bureaus and thus hurt your credit score.

Credit utilization, meanwhile, refers to the amount of credit you use compared to your available balance. For example, let’s assume you have three credit cards; the aggregate credit limit is $10,000, and the current balance is $3,000. In this case, your credit utilization rate would be 30% ($10,000/$3,000). Many experts recommend keeping your credit utilization rate below this percentage, so do your best to make extra payments every month.

Some other factors that matter include the age of your accounts (the longer your accounts are open, the better), your credit mix (loans versus credit card accounts in your name, knowing a combination is best), and the length of time that’s passed since you applied for new credit (each new application may shave a few points off your score).

Why do I have different credit scores?

Keep in mind that having the same credit score with all three bureaus is unusual as each one calculates this a little bit differently. As previously mentioned, bureaus also rely on lenders to submit data: meaning that if one bureau doesn’t receive data as quickly as another, they’ll produce a slightly different score.

Credit scoring companies also exist outside the three bureaus—with FICO and VantageScore most often used by lenders—and calculate their scoring models (mathematical formulas) using the same underlying data from credit reports to determine your credit score.

So, what does this all mean for you? If you’re looking for a single “real” credit score, you can end your search because this is, quite frankly, impossible; and if you’re shopping for a loan/applying to different lenders, know that each will score you a bit differently depending on the models used. Among all companies and scoring models, however, one commonality exists; they all agree on the significant factors that impact credit scores (as discussed in the previous section).

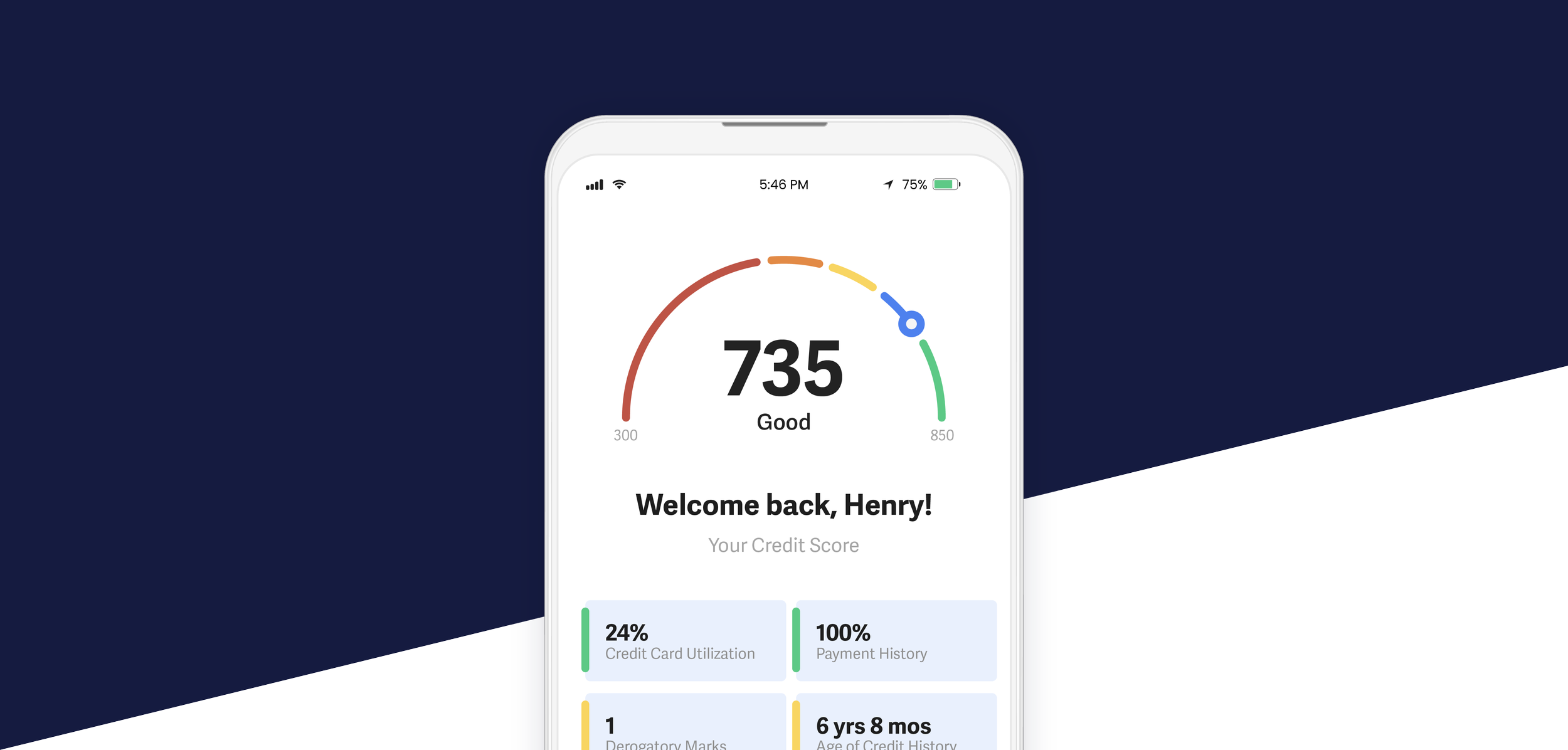

What is a “good” credit score?

The answer to this question depends on the credit scoring model used (sorry, we promise we’re not trying to overcomplicate the topic). For example, many lenders use base FICO scores while auto lenders and credit card issuers use industry-specific FICO scores—with various versions of each model. Compounding the confusion is that each model features a different range; base FICO scores have a range of 300 to 850 while their industry-specific counterparts range from 250 to 900. The good news, however, is that classification groupings are generally the same:

FICO Chart:

Source: Experian

VantageScore—another common score lenders rely on—also features diverse credit scoring models. As with basic FICO scores, two of the company’s most recent models use a 300–850 range:

VantageScore Chart:

Source: Experian

For reference, most lenders require a minimum credit score of 620 to purchase a home with a conventional mortgage (meaning one not backed by a government agency, such as from a bank or credit union).

How does my credit score affect my ability to get a loan?

At the end of the day, lenders want to reduce any potential risk they might incur by taking you on as a loan holder; credit scores help creditors not only predict an individual’s level of financial consistency but also serve to hold individuals accountable if and when they fail to make payments on time.

A poor credit score may result in a loan application denial, which can also occur if other eligibility requirements are not met; and while you can still receive a loan with a less-than-excellent score, this will likely result in a higher interest rate: making monthly payments significantly more expensive.

How to improve your credit score

If you’re already grappling with a low credit score, you know just how challenging it is to climb out of that hole. Fortunately, however, improving your score is not as impossible as it may seem.

First, it is important to not miss any payments and catch up on any past-due accounts—as late payments can remain on your credit report for up to seven years. If you’re drowning in credit card debt, seeking counseling services is often beneficial as a counselor can sometimes negotiate lower rates and payments while working with card issuers to bring your accounts current.

On a similar note, it’s best to keep your credit utilization rate as low as possible; as a benchmark, those with the highest credit scores tend to keep this number in the single digits.

Finally, you’ll also want to limit how often you apply for new accounts—as each inquiry can ding your credit score.

How to check your credit report

If you’re looking to obtain a loan or are simply interested in maintaining your financial hygiene, it’s important to check your credit report at least once a year to stay up to date. After all, credit reports are an important metric for lenders—so it’s best to know how you look on paper and then take measures to improve if need be.

An additional benefit of checking your credit report on a regular basis is that you may be able to spot signs of fraudulent activity. Millions of Americans unfortunately fall victim to identity theft every year, a crime that is often time-consuming and costly to resolve. By keeping an eye on your credit report, you may be able to catch a fraudster before he or she completely wrecks your credit score. All three credit bureaus offer a free credit report every 12 months, so it’s best to take advantage of this whenever the opportunity arises.

In sum: what you should know about credit scores

Now that you’re well-versed in the language of credit scores, we hope you’ll feel more confident when speaking to a lender or—at the very least—at your next social gathering.

Have questions about credit scores? Schedule a FREE discovery call with one of our CFP® professionals to get them answered.

———

Vision Retirement is an independent registered advisor (RIA) firm headquartered in Ridgewood, New Jersey. Launched in 2006 to better help people prepare for retirement and feel more confident in their decision-making, our firm’s mission is to provide clients with clarity and guidance so they can enjoy a comfortable and stress-free retirement. Schedule a no-obligation consultation with one of our financial advisors today!

Disclosures:

This document is a summary only and is not intended to provide specific advice or recommendations for any individual or business.